Cost Inflation Index

CA Dhyey Shah

11/6/20251 min read

The Central Board of Direct Taxes (CBDT) has notified the Cost Inflation Index (CII) for the Financial Year 2025-26 as 376, vide Notification No. 70/2025 dated 01 July 2025.

The Cost Inflation Index is used for computing Long-Term Capital Gains (LTCG) on the sale of capital assets such as land, buildings, certain mutual funds if purchased before 23rd July 2024. It adjusts the purchase price for inflation, ensuring a fair and equitable calculation of taxable income.

Under the new capital gains regime introduced through the Finance Act, 2024, indexation benefits are available only for assets purchased before 23rd July 2024.

Hence, taxpayers who have acquired capital assets on or before 23rd July 2024 can continue to use the CII = 376 for FY 2025-26 while computing long-term capital gains.

Example:

If a property was purchased in FY 2015-16 when the CII was 254 and sold in FY 2025-26, the indexed cost of acquisition will be:

Indexed Cost = (Cost of Acquisition × 376) / 254

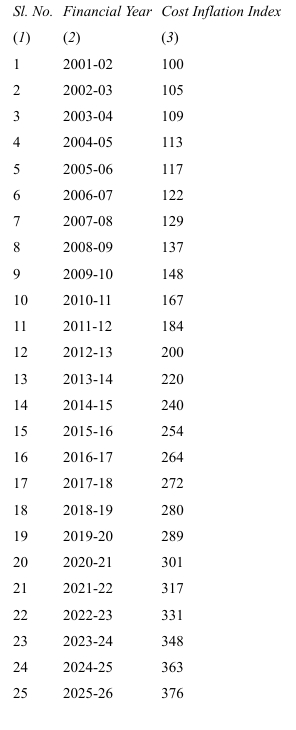

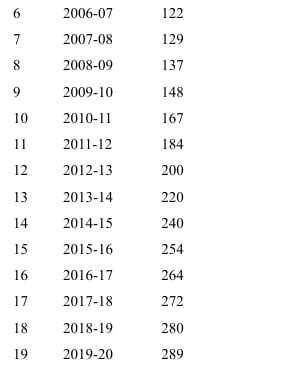

The following are the Notified Cost Inflation Index under section 48, Explanation (V):

Disclaimer:

The above information is intended for general awareness purposes only and does not constitute professional advice. It is not exhaustive in nature and may be subject to amendments or interpretations by the authorities. Before making any decisions or taking action based on the contents of this article, readers are strongly advised to seek professional guidance from a qualified Chartered Accountant.

Quick Links

Contact

info@cadhyeyshah.com

© 2025. All rights reserved.

GF 6, M Square Building,

Near Dominos Pizza,

Swastik Society,

Chimanlal Girdharlal Road, Near City Centre

Navrangpura, Ahmedabad - 380009