Changes in Small Company Defination

CA Dhyey Shah

12/2/20251 min read

Change in Limits of a Small Company:

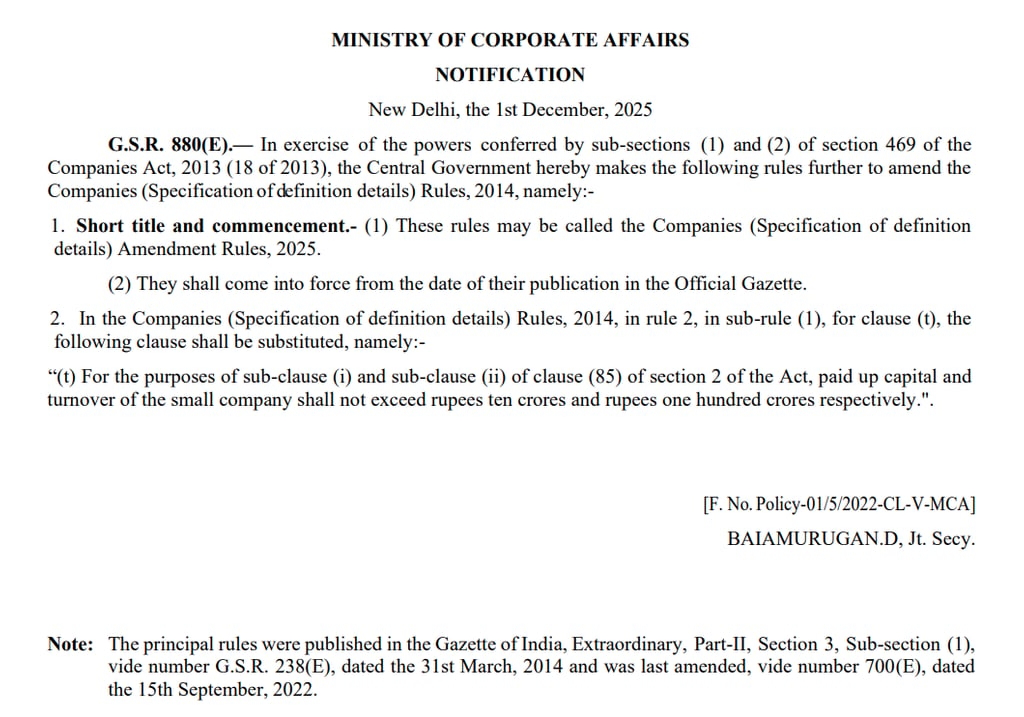

The Ministry of Corporate Affairs (MCA), vide Notification No. G.S.R. 880(E) dated 01.12.2025, has amended the limits prescribed under Section 2(85) of the Companies Act, 2013 for classifying a company as a Small Company as below:

Paid Up Share Capital shall not exceed

Revised Limit (Effective 01.12.2025): 10 Crores ₹

Old Limit: 4 Crores ₹And

Turnover (as per previous year Profit & Loss) shall not exceed:

Revised Limit (Effective 01.12.2025): 100 Crores ₹

Old Limit: 40 Crores ₹

These enhanced thresholds significantly widen the eligibility criteria, bringing many more companies under the “Small Company” category.

Major Benefits Available to Small Companies:

1. Board Meetings

Only two Board Meetings in a year (one in each half, minimum 90-day gap) instead of the usual four.

2. No Mandatory Cash Flow Statement

Financial statements need not include a cash flow statement.

3. Simplified Annual Return

MGT-7A - It can be Signable by CA or CS.

4. Exemption from CARO

Small Companies are not covered under the Companies Auditor’s Report Order (CARO).

5. Lesser Penalties

Small Companies enjoy reduced penalties for certain defaults.

The revised thresholds under Section 2(85) (effective from 01.12.2025) represent a significant step toward simplifying corporate compliance. With increased limits of ₹ 10 crore paid-up capital and ₹ 100 crore turnover, a much larger number of companies can now operate with reduced regulatory burden, enhanced flexibility, and lower compliance costs.

Quick Links

Contact

info@cadhyeyshah.com

© 2025. All rights reserved.

GF 6, M Square Building,

Near Dominos Pizza,

Swastik Society,

Chimanlal Girdharlal Road, Near City Centre

Navrangpura, Ahmedabad - 380009