Changes in GSTR 9 & 9C - FY 2024-25

Key Changes

CA Dhyey SHah

11/26/20252 min read

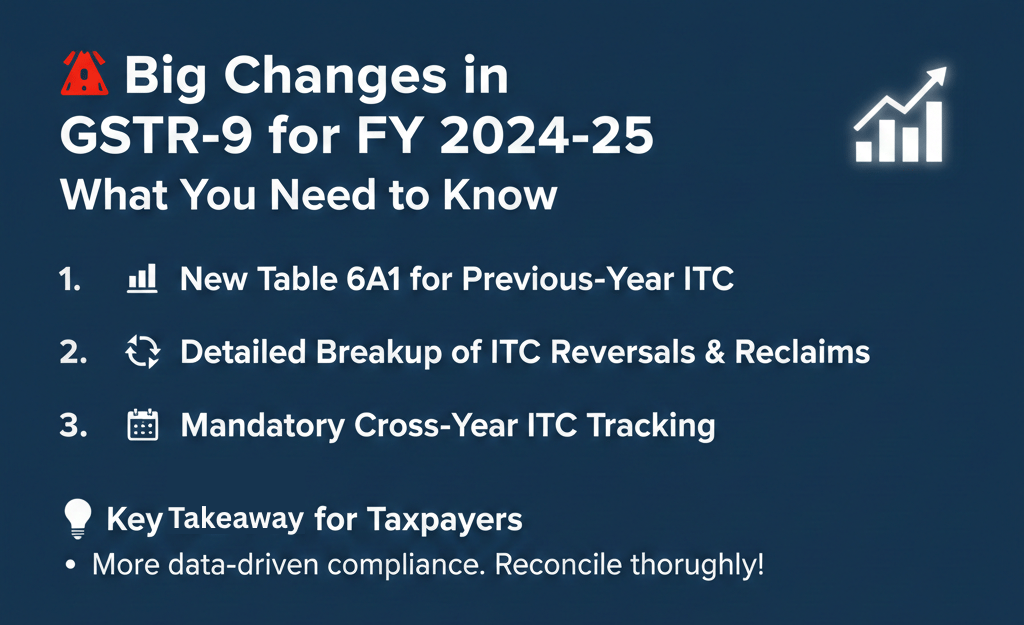

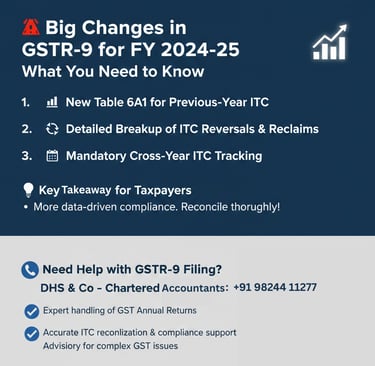

🚨 Big Changes in GSTR-9 for FY 2024-25: What You Need to Know

The CBIC has introduced sweeping updates to GSTR-9, the annual GST return, making ITC reporting far more detailed and transparent. Here are the key changes and why they matter:

1. New Table 6A1 for Previous-Year ITC 📊

A fresh row, 6A1, captures the ITC carried forward from the previous financial year (i.e., FY 2023-24) that was claimed in FY 2024-25.

This helps separate old credits from current-year transactions and reduces confusion.

Another auto-calculated row, 6A2, now shows the “net current-year ITC,” calculated as (6A – 6A1).

2. Detailed Breakup of ITC Reversals & Reclaims 🔁

Split ITC Reversals: Reversals of ITC must now be reported in separate, specific tables based on the relevant rule:

Rule 37 (non-payment to supplier within 180 days) is reported in Table 7A.

Rule 37A (supplier does not file GSTR-3B) is reported in Table 7A1.

Previously, these could be aggregated, but separate reporting is now mandatory for better audit trails.

Explicit Reclaim Reporting (Table 6H): A new Table 6H is used to report ITC that was previously reversed (e.g., under Rule 37/37A) and has been subsequently reclaimed in the current financial year.

3. Mandatory Cross-Year ITC Tracking (Tables 12 & 13): Tables 12 and 13, previously optional, are now mandatory if applicable.

Table 12: Reports the details of ITC for FY 2024-25 that was reversed in the subsequent financial year (FY 2025-26).

Table 13: Reports the details of ITC for FY 2024-25 that was availed for the first time in the subsequent financial year (FY 2025-26) (up to the October 2025 GSTR-3B filing).

This mandatory reporting ensures precise tracking of cross-year adjustments and prevents irregular ITC claims.

📊 Other Notable Amendments

Beyond ITC, several other structural changes affect reporting requirements and processes:

Detailed Tax Discrepancy Explanations: Table 9, which deals with tax liability and payments, now requires detailed explanations for any variances between the tax payable and the amount actually paid, with a clear split between cash and ITC utilization.

New Reporting for Import IGST: Table 8H1, new disclosure requires reporting of IGST paid on imported goods where ITC is claimed in a next financial year, helping track delayed claims.

💡 Key Takeaway for Taxpayers

These changes signify a move by the tax authorities toward a more data-driven compliance regime, with an emphasis on granular detail and transparent reconciliation. Proactive preparation and thorough reconciliation of your books of accounts with GSTR-1, GSTR-3B, and GSTR-2B data are crucial to ensure smooth filing and avoid potential notices or penalties.

📞 Need Help with GSTR-9 Filing?

· For professional assistance in GSTR-9 filing, GST reconciliation, audits, and compliance-related queries, you can connect with:

DHS & Co – Chartered Accountants

✅ Expert handling of GST Annual Returns

✅ Accurate ITC reconciliation & compliance support

✅ Advisory for complex GST issues

📱 Contact: +91 9824411277

Quick Links

Contact

info@cadhyeyshah.com

© 2025. All rights reserved.

GF 6, M Square Building,

Near Dominos Pizza,

Swastik Society,

Chimanlal Girdharlal Road, Near City Centre

Navrangpura, Ahmedabad - 380009